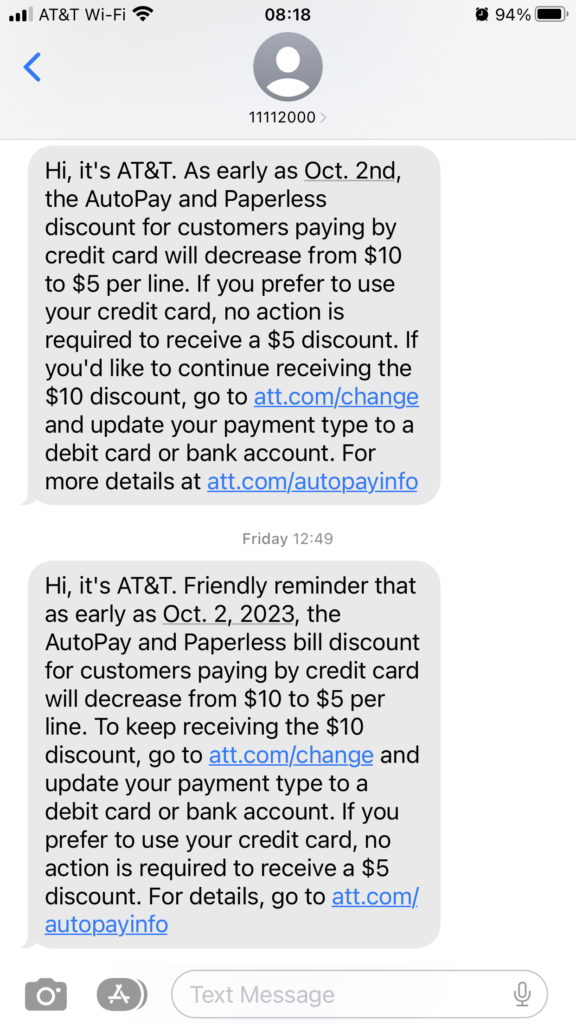

A couple of months ago, I got a text message from AT&T indicating they were intending to lower the “discount” for paperless billing and automatic bill payment when using a credit card as the stored payment method.

Whilst I have no problems with electronic billing, ordinarily I’m not keen on “automatic payment” schemes when my credit union has a perfectly acceptable bill payment solution built into their banking portal. This forces me to keep a close eye on the bill and allows me to spot and deal with any potential billing problems before they become major issues.

However, it’s rather hard to walk away from quite a saving when the already massively bloated cell phone bill has six lines (though the maximum discount of $10/line topped out at five lines so once the sixth line came along, the discount was halved even though the plan will support ten lines being billed which was another screw job brought to you by AT&T! Thanks so much!).

The more I got to thinking about this, the more I’ve become convinced that not only was this change that was being imposed upon us very anti-consumer, it is actually at best a potential end-run round to violate credit card fee surcharging rules governing how merchants may pass credit card processing fees along to consumers that is part of their agreement with Visa and Mastercard International (and I’d imagine the other credit card brands as well) and may well actually be an illegal trade practise.

Credit Card Processing In A Nutshell

There is no doubt that most consumers love the convenience of using a credit or debit card to make a purchase. A tap or swipe and perhaps a signature or PIN and we’re on our way much faster than writing a cheque or fumbling for cash at the till.

What we don’t tend to think of is what’s happening behind the scenes to the merchant that accepts that plastic for your purchase.

I won’t go into all of the gory and arcane details of credit card processing here but in a recent journey of discovery on how I might accept credit/debit cards for my business, I was horrified to see the rather extravagant fees imposed upon merchants when the consumer uses their credit/debit card.

There’s a lot of moving parts in the system behind that innocuous terminal that you use your card (or your phone if your card is stored in the phone’s wallet) and a very complicated transaction that occurs behind the scenes between the bank that issued your card and the merchant’s bank that your payment will be deposited into with more than a few additional entities between those two banks who will help themselves to a slice of the payment to facilitate the exchange.

Often this “merchant fee” or “payment processing fee” will be in the form of a percentage (which usually comprises the merchant payment processor’s fee and the interchange fees imposed by Visa and Mastercard et al plus a fixed amount) which can vary depending on how the card is accepted or a flat rate or even both. Generally, the percentage fees are noticeably higher for transactions that are done without the card being present (i.e. card details stored in the merchant’s system or manually keyed) versus those where the customer physically swipes/dips/inserts the card into a terminal.

The fees can vary wildly depending on the processor and the volume of payments you’re pushing through their payment network but for us small merchants, payment processing fees of 2.3-3.2% + 30 cents for card-present transactions and 3.6% + 30 cents for card not-present transactions seem to be the prevailing standard as of this writing and these rates are subject to change often.

So for a $100 charge on your card that you swiped through their terminal, the merchant would only see $96.80 deposited in their account assuming a 2.9% + 30 cents processing fee which is about the mid-point of rates easily obtainable by merchants that aren’t high-risk or luxury vendors.

A Brief History of Credit Card Surcharging

As you can imagine, it was rather horrifying discovering just how much banks/credit card processors would be helping themselves to money they had nothing to do with earning.

Most merchants would love to pass along that cost to the consumer rather than eat it as a cost of doing business which is shaved off the top of the transaction hoping that volume or price adjustments will still allow them an acceptable profit.

For many years, merchants were generally prohibited from surcharging credit cards by most states with laws prohibiting the practise until the merchants filed a class-action lawsuit in 2005 that was eventually settled allowing surcharging to start in 2013 so that as of 2023, only Connecticut, Massachusetts, and Puerto Rico outright ban credit card surcharging.

Credit card surcharging is subject to the following rules/principles:

- Merchants wishing to pass along the surcharge to their customers had to notify each credit card brand (like Visa or Mastercard) at least 30 days before implementing the surcharge.

- Merchants had to have clear signage at the point of sale showing the credit price or the credit and cash prices as well as informing the consumer that credit card users would be charged the processing fee as a separate line item surcharge. Debit cards and pre-paid cards are not allowed to be surcharged and the payment terminal and/or processing back-end has to figure out if the card is a credit card or debit card (and the consumer selecting “credit” for a debit card on the terminal has nothing to do with this…that only dictates if the transaction is a signature or a PIN-based transaction).

- Merchants would not be allowed to profit by surcharging more than their actual processing fee imposed by the processors and in no case can the surcharge exceed 4% of the transaction total (and in Visa’s case, the surcharge is capped at 3%).

There are a few other rules and minor tweaks based on jurisdiction but those are the main ones and it is that last one in particular that brings us to why I think AT&T’s move is at best anti-consumer and at worst illegal.

AT&T Joining The Race To The Bottom

AT&T has decided that their competitor’s exceptionally poor idea of trying to force people to use debit cards or their bank’s Automated Clearing House (ACH) details to allow the phone company access to their bank account is a move they wish to match.

It’s been clear as day (and much clearer than the signals on the telephone lines!) throughout my life that the phone companies really do not like their customers and could really care less about what would be best for consumers. One of the more famous skits from when Saturday Night Live was actually relevant is on point in 1976 and the attitude from the phone company hasn’t really improved since they were regional Bells to “Ma Bell” AT&T owning them all as a monopoly and then the split back to the regional Bells only to see consolidation and chaos ever since!

And don’t think we didn’t notice that subtle connection between Lily Tomlin playing Earnestine the Operator and the current main spokesperson for AT&T. Deep down in the bowels of AT&T, the spirit of Earnestine is alive and well and sometimes it’s right in our faces! 🙂

Anywho, it’s a horrifyingly bad idea to force consumers to switch their preferred payment method from credit cards which are relatively painless to sort out unauthorised/duplicated billing to debit/ACH which allows the phone company to potentially empty your account if the billing system decides to have a really bad day.

If they do that to a credit card, it often takes a phone call to a rep (or more often now you can dispute the charge online) and generally it goes away in a couple of days.

Good luck getting your money back into your bank account if they’ve taken more than you actually owe in less than a week. More often it takes months involving several phone calls to rather disinterested reps who conveniently forget the last month’s conversation (and the months before that) before they finally take the hint. And all the while your money and good character are held hostage until the phone company and/or the bank finally decides to sort out the problem they’ve created.

If that wasn’t bad enough, now imagine your bank account details being stored on their servers.

Does that scare you?

It ought to in a modern era where it’s a rare week we’re not seeing a data breach being reported in the news…and that’s the breaches they actually admit to because someone stumbled upon it. More often than not, data breaches that occur are never reported to the consumer unless the company absolutely has no choice in it and even then that will be only when the potential fines and criminal charges outweigh covering up the breach.

Nine million AT&T customers had their data exposed in January 2023 but we only learnt of it in March. Fortunately, this time the breach didn’t involve credit card numbers or SSNs but the data that was accessed was still quite sensitive. Other breaches at AT&T weren’t quite so innocuous with financial details being leaked and offered up for sale by bad actors.

And it’s not like their competitors are all that hot at keeping hackers out of their billing databases. T-Mobile in particular has been breached twice this year (that we know of) with the first one exposing the billing details and Social Security numbers (amongst other highly sensitive data) on 37M customers!

Do you *REALLY* want your bank details in the computers of companies that have proven time and time again they suck at keeping the baddies at bay?

But Wait, It’s About To Get Worse!

Following the “lead” of T-Mobile and Verizon, AT&T is choosing to punish customers who prefer keeping their bank accounts safe from being drained by crims getting hold of their debit card information or the ACH details, the $10/month discount for paperless billing and automatic payment will be halved to $5/line per month.

Think about that carefully for a second.

Credit card users are going to lose half the discount to two features that dramatically reduce costs for AT&T by vastly reducing the amount of paper printed in the forms of bills and postage to send that bill through the mails to where it will hopefully be delivered properly to the customer (assuming their postal carrier isn’t as hopeless as the ones I’ve endured for the last 12 years but even though they attempted delivery when they felt like it which wasn’t often, they never seemed to misplace the bills as they have other things that have been posted to my end of the cul-de-sac).

And that’s not even talking about the massive saving in labour to open the envelope and process cheque payments that were returned through the post and wait for the payment to clear rather than have it transferred relatively quickly to their coffers via the card payment system!

To be fair, I’ve no doubt that eventually even AT&T’s “discount” for paperless automatic billing will be tossed to the bin because the phone companies have gotten used to pretty much getting away with as much price gouging as their forced arbitration clauses have allowed them to do so.

But to be honest, they could pay us $20/line per month for that feature and they’d still make a ginormous profit no matter how much they would howl in protest if they were forced to do that.

Just When You Thought Things Were Bad Enough…

Returning to the general rules for credit card surcharging given above and the fact that only credit card users are affected by this dramatic adverse change in the terms of service, when you do the maths it becomes readily apparent that the credit card users are really being screwed in what appears to be an end-run round the credit card brand’s rules on surcharging agreed as part of the consent decree that settled the class action lawsuit of 2005.

Let’s take the rules point-by-point, shall we?

- Notifying the credit card brand at least 30 days ahead of the implementation? There is no way to know if AT&T has done this and certainly none of the representatives you’d get on the phone or the chat-bot would answer that question even if they could. However, the amount they’re effectively surcharging being well over the permitted amount in most jurisdictions including mine of North Carolina would suggest they’ve not made an attempt to notify the cards of the intent to surcharge.

- Clear signage informing consumers of the surcharge for using a credit card: the text messages and other official communication probably satisfies that requirement even though AT&T refuses to admit that the halving of the discount is effectively a surcharge in disguise with a different name.

- The company cannot profit from the surcharge and charge more than their actual cost and no more than 4% in total surcharges?

They fail that last test miserably.

My current bill is $295/month covering six lines and a tablet and all of the junk fees and taxes.

At six lines looking at an effective increase of $30/month by halving their current $10/month discount for those lines to $5/month for the paperless automatic billing, this works out to be an effective surcharge of 10% which is *WELL OVER* the 4% maximum allowed surcharge (and it’s even worse because the credit card in question is a Visa card which limits the surcharge to 3% maximum or the amount actually imposed by the payment processors).

And that’s assuming AT&T was paying retail merchant payment processing rates that any business owner could. The actual amount AT&T spends to process a credit card is likely *FAR LESS* than the example I gave because with their processing volume, they could negotiate a much more favourable processing rate than many of us could ever hope to dream of! If they were truly paying the retail processing rates, then they’re either grossly incompetent and can’t negotiate their way out of a paper sack or they genuinely don’t care that their already egregious profits could be even higher.

With their quarterly turnover, they could probably buy a bank or two or some payment processor like Square or Stripe for cash and have them do their in-house processing for peanuts.

At the very least, that surcharge well in excess of the cap is a gross violation of their merchant agreement with Visa International when it comes to the rules governing surcharging.

It’s even more egregious that in order to preserve the discounts AT&T and I had *ALREADY AGREED TO* in an relationship that is already decidedly one-sided and getting worse all the time, I’m expected to allow AT&T direct access to my bank account and assume all of the risks inherent to that with no assurances any errors will be made right in a timely fashion?

Not only no, but *HELL NO*!

Yes, I know the subscriber agreement has clauses that allow them to unilaterally change the terms when they feel like it with notice but just because they can unilaterally enrich themselves with no consideration to or for the customer does not make it moral or just for them to abuse that power whenever they feel like it because they know that regulating their piss-poor corporate behaviour toward their customers is a joke at best and that the consumers really don’t have any truly better options when everyone else is implementing the same sorts of anti-consumer policies.

In The Interest Of Fairness…

Once it became obvious to me that this move by AT&T seemed to be a back-door surcharge, I figured it was only fair to see if AT&T had any comment on the proposed changes.

If I’m ultimately planning to go the formal complaint route, then were I them I’d want the opportunity to at least give the company’s perspective to try to convince the consumer otherwise.

That was the mindset that had me ring up the AT&T 1-800-U-A-Loser “customer service” phone line round noon which connected me to an obviously foreign call centre staffed with people whose accents and inflections strongly indicate they were located in the Philippines.

The following are my notes of that conversation:

- After a couple of minutes on hold, I’m connected to “Carla” who is obsessed with a “security code”. AT&T put this code on my account many years ago and to this day I still have no idea what it is which usually entails a few minutes of argument before the representative finally sends a one-time code as a text message to my phone (but only after I gave her “consent” to send the code which is more than a little odd when the entire argument was to find a way to satisfy her farcical obsession for “security” and the one-time text message code was the only way to proceed…I don’t exactly have a choice but to consent, eh?).

- Carla clearly is not a native speaker of English and the only way she was at all coherent was her reading from prepared scripted responses. Her comprehension of clearly spoken Queen’s English (sorry, now it’s the King’s English…God help us all with that twit on the throne of St Michael and St George) was even more lacking.

- At the 10 minute mark, Carla finally gives up in favour of finding a supervisor but to no one’s surprise, they’re all in a meeting and are unavailable. I decline the offer of leaving a voicemail message I know will never be returned and suggest we can wait for the supervisor to turn up.

- In the mean time, I ask Carla if she can determine if a card is a credit card or a debit/prepaid card with just the numbers of the card, the expiry date, and the CVV2 code. The short answer is that you can’t as only the payment processor’s back end will be able to determine that when it goes through the machinations of the transaction. Carla doesn’t seem to understand this could potentially lead this backdoor surcharge being inappropriately applied to debit/prepaid cards which is explicitly forbidden by the rules if the surcharging scheme isn’t implemented properly. This is why they require prior notice and must configure surcharging on their end so that the payment system can compute the surcharge appropriate to the type of card.

- 46 minutes: on hold again.

- 51 minutes: Carla comes back on but it’s more of the scripted party line.

- 53 minutes: on hold again.

- 56 minutes: the presumed supervisor named Brix (I kid you not!) finally turns up and takes over the call.

- When pressed for why AT&T was punishing credit card users only, Brix offered the party line that AT&T had noticed an increase in credit card reversals as well as late payments but when pressed on what percentage of credit cards were proving problematic, he refused to answer leading me to believe that the percentage is far lower than would justify an across-the-board credit card penalty for “increased processing costs”.

- If customers initiating charge-backs inappropriately to avoid paying a legitimate bill were truly a problem, AT&T would have plenty of options at hand that would be perfectly legal and certainly much more fair than levying a penalty well above the proscribed limits on every credit card user:

- AT&T could lock down that problematic customer’s account so that they would have to use a debit card or ACH or pay at their authorised retailers (which if memory serves incurs another fee).

- If that didn’t mend the customer’s ways, they could certainly sue the customer in small-claims court for defrauding the merchant in a way that would be tantamount to bouncing a cheque. Non-sufficient funds (NSF)/bouncing cheques is subject to bank fees and in some instances treble the face amount of the cheque as damages.

- If the customer is truly hopeless or unwilling to pay their bills appropriately, then AT&T could well suspend and/or terminate their service which I’m reasonably sure would get the customer’s attention.

- If none of these remedies works and the customer skips out on the bill, AT&T would be well in their rights to write the bad debts off their taxes. I really have a hard time seeing where AT&T really loses in this scenario!

- A debit card and/or ACH bank details is no guarantee that the bill will be paid any more than a credit card is and is even more likely to end up with a potential NSF than credit cards where the customer more often than not would have sufficient credit available which could be held/frozen when the credit card charge is put through and that answer comes through immediately. The big difference is that a customer making a mistake with a credit card is an OOPS that’s relatively painless to fix whereas mistakes where a live bank account are concerned are far more problematic and often take much longer to resolve.

- If customers initiating charge-backs inappropriately to avoid paying a legitimate bill were truly a problem, AT&T would have plenty of options at hand that would be perfectly legal and certainly much more fair than levying a penalty well above the proscribed limits on every credit card user:

- I also pressed Brix on whether AT&T would commit to any performance guarantees that would require them to refund inappropriate debits (double-billing) in a timely fashion similar to that which is customary when disputing a credit card charge. Brix’s take was that AT&T would not guarantee any resolution.

- I asked Brix how timely and comprehensive a response and restitution from AT&T could be expected if the inevitable data breach to come compromised the debit/ACH details to crims who then emptied the account of funds. It seems the customer is completely on their own in that situation as well.

- I did suggest that he might want to forward these concerns up the chain of command (if not send a copy directly to CEO Stankey) but I have zero confidence that would have happened.

- 1 hour 45 minutes: finally disconnected.

As it turned out, my oldest son’s phone decided it wasn’t interested in being a phone and preferred the cellular afterlife as an Apple-branded brick so I had the opportunity to pick up his new phone from the AT&T store.

Whilst there, we again had the pas-a-deux dance about the security code that I *STILL* have no idea what it is but at least we got to the one-time text code much faster and the rep then changed the code on his back-end but never told me what number he changed it to.

I raised these points to the manager on duty who had only become aware of AT&Ts desire to change the discount scheme in the past couple of days by other customers coming in and making enquiries about it. He had been provided no official papers or party line but after taking him through the same arguments presented above, he did agree that one could interpret the change as an illicit credit card surcharge.

Sadly, his revelation and vastly increased knowledge of payment processing won’t make it any further as apparently the AT&T operations folks rarely listen to the feedback from the front lines.

Quelle surprise.

Where Do We Go From Here?

The problem is that I truly have no idea who would have jurisdiction over at least getting AT&T to answer (and hopefully reverse but I don’t hold out hope for that given how hard they’re fighting the class-action arbitration for their utter BS per-line “administrative” fee) for what appears to be a back-door surcharge scheme that violates the most important rule that merchants may not profit by surcharging.

The Federal Communications Commission (as a billing issue)?

The Federal Trade Commission (for deceptive and unfair trade practise)?

The North Carolina Attorney General (for price gouging and unfair trade practise)?

Visa and Mastercard International (and perhaps Discover and AMEX) for violating the surcharging rules?

Of those four, Visa seems the most determined to punish merchants who violate the surcharging rules but AT&T would likely argue that a “discount” is not a “surcharge” even though I think the reasonable man in the street would agree that if an increased cost is being borne only by those who choose to use a credit card for payment, then regardless of what you may *CALL* it, it is a credit card surcharge in actuality and should be subject to the rules that were agreed by the payment industry.

When the only people being affected are those who use credit cards and they’re having to pay much more to use that credit card for payment than they have in the past, that’s a surcharge.

Does anyone in North Carolina really believe that the Highway Use Tax isn’t the sales tax by a different name?

Or the Use Tax imposed on Form D-400 on a personal return which happens to be the exact same percentage as the sales tax rate in your county isn’t in fact the sales tax by a different name?

You could at least argue the first one is earmarked for the NC DMV budget bucket but the second one is clearly an imposed sales tax identical to the same one you’d pay at the till in the shoppes on the High Street.

I’ll let you know because I intend on sending this deep dive to all of them and let whoever cares to pursue it assert their jurisdiction because goodness knows a month of research has made me wonder who truly will take up the fight for the consumer with AT&T.

I’m not holding my breath that they will stop AT&T from implementing this anti-consumer policy in violation of the merchant agreements they signed to accept credit cards.

But I would welcome being proven wrong. 🙂