Even as jaded about how awful customer service these days can be and how it’s the most likely cause of death the coroner will ascribe to me when that day comes, I have to say that today’s “adventure” trying to seek redress of the erroneous imposition of a “foreign transaction fee” to the renewal of this web hosting package for another year really stands out for just how much stupidity was enshrined into policy and process that’s shepherded along by arguably some of the most moronic imbeciles outside of the credit reporting industry.

Let’s just say I totally understood John’s frustration as reproduced in the real complaint letter he sent to NTL (below) and whilst I didn’t alleviate my boredom in the way he suggested, I’ll admit there were times I’d have likely found it far more productive and meaningful had I done so.

Any bank can make a mistake!

In an industry that processes billions of transactions per day, it’s not too much to imagine that the occasional mistake will slip through the cracks to vex the poor souls who are afflicted by them.

Unfortunately, the bank that Intuit chose to back their Quickbooks Checking and Quickbooks Payment services (among others) is none other than the rather notorious Green Dot Bank which has had quite the chequered history for dodgy behaviour when it comes to properly processing transactions and an alarming tendency to capriciously hold depositor’s money hostage.

I can only imagine that Intuit chose that lot because they were the cheapest vendor willing to give Intuit cover from being regulated as a financial institution themselves and the dodgy behaviour of Green Dot Bank.

I should have taken the hint when Quickbooks Checking and Green Dot completely screwed up the payment of the fibre internet bill but I chalked it up to the debacle that was Google Fibre upgrading a perfectly functional billing system to an “improved” one I never requested that clearly had zero testing before it went live and was a two-month nightmare (film at 11!).

I genuinely had no idea that Green Dot would actually live up to their horrible reputation as being even more evil and despicable than the “Bank of Evil” Gru goes to finance his rocket so he can shrink the Moon and hold it for ransom!

So what went wrong here?

The web hosting package that powers this and my other websites is paid on an annual renewal basis.

I’ll give a huge shout-out to Shock Hosting as they’ve been pretty much the easiest reseller web hosting to maintain I’ve ever had and it just plain works.

I don’t have to babysit AutoSSL as I did at previous hosts which failed to auto-renew the SSL certificates that provide encryption for web traffic nor did I have to deal with the very nasty and prolonged upgrade of the underlying server OS I was facing at my last web host which I otherwise loved but had been priced out of using.

Shock Hosting has servers all around the world but they’re an American company operating as a Limited Liability Corporation (LLC) which is a corporate structure rather unique to American business corporation law. The UK and other countries do have the concept of a limited liability corporation (in the UK, you can tell those at Companies House designated as Ltd after their name) but the LLC designation is definitely American.

Shock Hosting’s corporate headquarters is in Piscataway NJ which, last time I checked, is still a city and state in the jurisdiction of the United States.

The websites are hosted on servers that are located in the United States and the contract for hosting is between two US entities.

So imagine the unpleasant surprise when I saw a bogus “foreign transaction fee” when the renewal was processed against the Quickbooks Checking account!

Solving this problem really doesn’t need to be so difficult!

Normally, all one needs to do to dispute a transaction through a reputable bank is log onto their web portal, mark the fraudulent transactions and perhaps fill out an online form and provide evidence (in this case, the invoice showing both parties are clearly in the United States) and that’d be the end of it after whatever “investigation” the bank might deign to do.

The law gives them an inordinate amount of time (up to 90 days) to conclude such an investigation but they rarely take more than a couple of days for the fraudulent charge to be reversed and the onus now put upon the entity that caused it to prove that it’s actually valid.

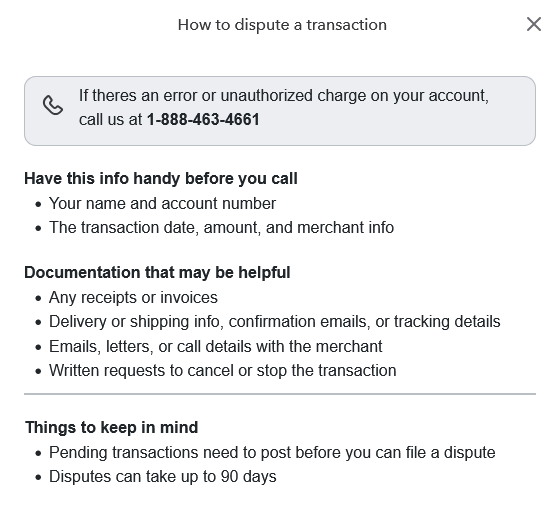

And looking at the user interface…there is no button to dispute a fraudulent charge.

Wonderful.

Instead, you get this popup on how to dispute a charge…

Immediately seeing a typo in the highlighted section (“theres” as opposed to “there’s” or the more professional “there is”) does not exactly fill one with confidence about the competence of the people with whom I’m likely to have an unpleasant conversation.

But as we’ll see, that was the least of the problems with this process…

Calling “Customer Service” as directed was a huge mistake…

The first person I get is someone named Rachel who seemed pleasant enough but upon being told what the problem was and that the foreign transaction fee needed to be disputed made it clear that her call centre has no power to fix the problem and that I’d have to speak to Green Dot Bank directly.

The only problem is that there’s really no way to contact Green Dot Bank on a direct line because the call centre Rachel wants to route me to is in India.

But before she will do the transfer, she wants to put me through a “verification process” even though she’s already identified me via caller ID.

Having experienced that trap before of being “verified” only to be “verified” again with the same questions by the agent I get transferred to by her, I suggest to Rachel that if I’ve got to go through the “verification process”, wouldn’t it make sense that I only do it once with the person who supposedly is the only one who can assist with this problem?

In fact, I have to make that suggestion three times before she finally takes the hint and passes me off to “Anthony” who, as expected, was going to put me through the same “verification process”.

Now…as someone who had an Uncle Tony who was 100% Hungarian and 0% Italian, I can tell you with absolute certainty that “Anthony” wasn’t Italian either.

An Italian, I can work with that because they have as little patience for bureaucracy and BS as I do.

But an Indian guy posing as an Italian even though he’s rocking a heavy accent strongly suggestive of Hyderabad or Bangalore instantly gives off a creepy vibe that I’m talking to someone who moonlights as a scammer pushing the Microsoft or McAfee “tech support scams” that clean out your bank account with maybe a bit of down on his luck Nigerian prince action on the side.

That grody feeling wasn’t helped when he wanted to verify my first and last name (OK, no problem there) and…my date of birth?!?

Who in their right mind designs a lookup system that is so easily confused by false positives?

I understand law enforcement officers will use that combination when they’re running someone for warrants or try to to catch them out for providing false info but normally you’d think a bank would go for information that isn’t readily available to the average person (like a unique account number or info that only the real person they’re trying to verify would know?).

I’m already feeling that this guy is pretty sketchy and that feeling doesn’t improve when he demands the ZIP code (yet another piece of data easily available to a hacker/scammer in thousands of leaked datasets through the years).

Where I draw the line with “Anthony” is when he wants the last four digits of the SSN.

I understand that banks are utterly addicted to the SSN as “identification” regardless of the fact that it’s known to be not unique (because Social Security has reissued numbers), easily fat-fingered because there is no check digits or other ways of verifying the number is correct, and combined with the date of birth and location you were born makes the other five digits of the SSN easily guessed in most instances (but thankfully not mine!) by even a low-powered computer.

But there is no way I was going to willingly give “Anthony” who has exhibited strong scammer vibes the last tool he needs to steal my identity and I ask to be transferred immediately to a US-based representative where I at least have a modicum of a chance of holding them accountable for violating laws and regulations concerning confidential information.

He flat out refuses to do so unless I give in to his blackmail demand for the partial SSN.

Put a pin in that because we’re going to come back to it later in this story.

But for now, I’m so over “Anthony” and let him be serenaded by the dial tone as I ring off.

Calling them back was an even worse mistake…

My hope at ringing them back straightaway was to go through this moronic “verification process” with someone who was at least based in the United States and I get someone whose name was something like “Khimia” but she was not the most easily understood.

I first ask her to get me to the US-based Green Dot call centre but she says there’s no way to do so…I have no choice but to go through the Indian call centre first.

So then I change tack and ask her that if I go through the stupid “verification” with her, will that at least prevent me from having to do the “verification process” again with the Indian agent she transfers me to who are giving off strong scammer vibes?

That’s when she confirms that my suspicion when I was talking to Rachel was actually correct that whether I do “verification” with her or not, I’m still going to be subjected “verification” by the Indians I clearly cannot trust as far as I can throw them.

Only this time, she refuses to pass me along to hopefully a different Indian with a much better attitude and a whole lot less scammer vibe until I submit to “verification” with her even though it’s completely useless and a waste of time.

Even though this “verification” is supposed to be a uniform process…she demands first name, last name, and…phone number?!?

Ah, wonderful…let’s let the tele-spammers have a go at me as well as the identity thieves. I guess I’ll be discovering how much better iOS 26 is at suppressing them than iOS 16!

Four minutes later, she shows how consistent the process isn’t by changing her demand to be for the EMAIL address associated with the account due to “recent policy changes” which I’d interpret as these people are making things up as they go along to merely amuse themselves at my expense.

“Sam” and the magic “left hand has no idea what the right is up to” trick!

Back to India I go and this time I get “Sam” who has just as strong a southern Indian accent who, as expected, demands I submit to his “verification procedure” when he refuses my request to transfer to a US-based call centre.

Seeing no option but to expose myself to the risk of identity theft thanks to Green Dot’s breathtakingly stupid policies and procedures, I first put it on the recording that I’m only complying under duress imposed by Green Dot and that should there be any identity theft or other schenanigans, they will be held liable to the fullest extent of the law.

I had to do this three times before “Sam” finally took the hint and understood the nature of a “question that only requires a yes or a no” and that proceeding to demand “verification” is very much presumed to be a YES on his part.

So I go through the “verification process” once again with someone who gives off slightly less scammy vibes (but frankly, only marginally!) and wait for him to fiddle about looking up things in the account.

He comes back after a couple of minutes and announces that he doesn’t have “permission” to dispute or reverse the foreign transaction fee that was applied in error.

Are you %^@*ing kidding me?!?

After all of that stupidity I was forced to endure to have to engage “help” from an Indian call centre I don’t trust and now you’re telling me that you after you’re the fourth in the line of people who have wasted a valuable hour of my time is not allowed to do the one thing I needed you to do?

Well, apparently not!

Even understanding that US corporations do not trust the offshore call centres to do anything of any import, this is an even more imperative reason why this function should not only never have left the United States and more importantly it should actually be a prohibited practice for any corporation in the United States to offshore call centre duties that handle sensitive information on American citizens.

What’s even more shocking to me is that the Senate had a bill in the first session of the 119th Congress (S.2495) and that the FCC is taking some time away from their current zealous abuse of the 1st Amendment rights of American citizens to propose a regulation that would largely do just that.

How “Ramon” was actually much worse than his four predecessors!

“Sam”, having proven how utterly useless he was transfers me to “Ramon” who frankly has a 50-50 chance of being in the United States or the Philippines.

At this point, nothing would really shock me about just how dire a state Green Dot’s operational standards are in at this juncture.

The fact that “Ramon” didn’t put me through the stupid “verification process” I’d already endured four times was one of them. Given Green Dot’s apparent addiction to that process that might well have been spawned from the Federal Reserve nailing Green Dot for a $44M fine for a laundry list of dodgy practices including lax verification and identification of money laundering (an illegal practice they tend to make shockingly easy to do!) was rather surprising:

WHEREAS, recent examinations of Green Dot, conducted by the Federal Reserve Bank

In re Green Dot Bank (Docket Numbers 24-005-B-SM, 24-005-B-HC, 24-005-CMP-SM, 24-005-CMP-HC)

of San Francisco (the “San Francisco Reserve Bank”) and the Federal Reserve Bank of Dallas

(the “Dallas Reserve Bank”) (collectively, “Reserve Banks”) identified certain significant

deficiencies relating to Green Dot’s compliance risk management framework, including, but not

limited to deficiencies in consumer compliance and compliance with applicable federal and state

laws, rules, and regulations relating to anti-money laundering (“AML”) compliance, including

the Bank Secrecy Act (“BSA”) (31 U.S.C. § 5311 et seq.); the rules and regulations issued

thereunder by the U.S. Department of the Treasury (31 C.F.R. Chapter X); and the requirements

of Regulation H of the Board of Governors to report suspicious activity and to maintain an

adequate BSA/AML compliance program (12 C.F.R. §§ 208.62 and 208.63) (collectively, the

“BSA/AML Requirements”)

Remember how I told you to remember that I’d asked “Anthony” to transfer me to a US-based call centre rather than give into his SSN blackmail?

“Ramon” tells me that I have the right to ask for a US-based representative at any time!

Oh, really? That worked rather swimmingly with “Anthony” who explicitly refused to do so even though “Ramon” thinks that it’s in their policy to do so when requested. It also didn’t work so hot when I tried to get past “Sam” who I’d guessed (and would be later proven right!) was useless who also blocked me unless I submitted to the “verification process”.

I proved conclusively that there is no direct number and no direct way to a US-based call centre and that “Ramon” was completely full of it. That does not inspire confidence in how the rest of this interaction will go.

Even more surprising was his take on who was responsible for applying the foreign transaction fee in the first place.

His first tack was to blame Shock Hosting and specifically their payment processor because “they have servers that are outside of the United States”.

Where their servers are located is irrelevant for the purposes of a bank levying a foreign transaction fee and their payment processor may not be and likely isn’t a bank as defined in the Banking Act of 1935.

Assuming for the sake of argument “Ramon” is correct that their payment processor is located outside of the United States which I’m awaiting verification from Shock Hosting in a support ticket to billing, it would not be surprising if Shock Hosting uses multiple payment processors throughout the world to support their worldwide hosting network.

But it beggars belief that they’d not use a payment processor based in the United States to service the billing between a US citizen/corporation contracting with a US LLC based in Piscataway NJ and the servers the hosting is located upon are in the NY/NJ area.

Nothing about that arrangement is indicative of anything foreign and indeed the previous two renewals were processed by that same LLC in the same location on the same servers and somehow didn’t incur a foreign transaction fee.

So what is more likely to be true? That a US-based financial institution had the possibility of increasing their profits with a foreign transaction fee for the past two years and didn’t (even as good as the bank in question is, they’re still a bank and still have a desire for profit) or that Green Dot has somehow misconfigured something on their end to flag the transaction as foreign even though it isn’t?

Green Dot’s own online reputation where a fair amount of the people who rated them with one star had the desire to choose zero stars or even negative based on their experiences with Green Dot imposing fees and freezing accounts before summarily terminating legitimate account holders without reason or recourse (with Green Dot often trying to hold onto the money before being forced to turn them over to the state’s escheat fund which is often not fun for a consumer to navigate if they even know it exists) should speak of the answer.

“Ramon” also seemed convinced that the foreign transaction fee was imposed by the payment processor and that Green Dot was totally innocent…they just apply the charges to the account and don’t bother with making sure it’s not actually warranted.

In so doing, he made the strongest argument that he clearly didn’t take the hint from the $44M fine referenced above and that Green Dot is apparently perfectly fine for being an easy vehicle for money laundering because it’s far more profitable to do so than the fine that’s supposed to dissuade them from engaging in such shoddy and illegal behaviour.

But “Ramon” also clearly doesn’t understand how the foreign transaction fee actually works and how it’s the paying bank that imposes the fee, not the payment processor or the merchant!

All the while saying that I don’t know how it works without having the faintest clue about my experience and background but I’d already clocked him as yet another incompetent imbecile working for Green Dot I cannot and will not trust to have a clue as to what he’s on about or anything he supposedly does unless it’s in writing.

You do a transaction with a foreign merchant, they process the payment and your bank receives the payment request in the preferred currency of the merchant. The bank then converts dollars to that currency at the prevailing exchange rate (usually LIBOR) and adds the foreign transaction fee on top of that to your statement as they ship the payment in the merchant’s currency off to the processor or the merchant’s bank.

That’s why you see both the original transaction and the separate foreign transaction fee…that fee came straight from your bank or card issuer, not the merchant or their payment processor!

“Ramon” supposedly keys in the dispute and I do eventually get an EMAIL proving he did…something.

Now where do we go (besides hell)?

Just when I thought the stupidity was done with after ringing off from “Ramon”, I check out the EMAIL thinking it’ll have a link to a secured portal where I could put in the details, attach the PDF of the invoice and just be done with it.

And you’d be completely wrong.

Green Dot apparently wants to make this process as byzantine and painful for the consumer they possibly can.

This is the point where I’d have been firing off copies of this missive to the Federal Reserve, the NC Attorney General (because we sure as hell can’t trust the ones we’ve had recently), and the Consumer Financial Protection Bureau if that hadn’t been destroyed by Elon Musk and his DOGE bros even though it routinely returned billions of dollars illegally stolen from American consumers.

The CFPB in particular paid for itself by the fines and the settlements it’d win against the banks and dodgy creditors and was reasonably effective at doing so (even though I’d not had good luck when they allowed Santander to unilaterally close a complaint I’d lodged against them).

This is exactly the reason why we need an independent agency with the resources capable of bringing the many bad actors in the financial industry to heel.

But back to the EMAIL…no portal to push the dispute and the evidence that Green Dot had completely screwed up and imposed a fee they have no legal right to impose.

No, I get a paper form I’ve got to fill out and put through the increasingly unreliable post in the next ten business days to somewhere near Philadelphia who may act upon it at some future point but somehow I suspect will still try to stonewall me and not give me back the money they unlawfully and fraudulently stole!

Intuit would be wise to find a much more competent and consumer-friendly company to provide banking and financial clearinghouse functions rather than likely the cheapest and shadiest vendor they could find that matches their own ethos to extract maximum profit with the worst possible customer service.

Somehow, I doubt that’ll happen anytime soon because birds of a feather tend to flock together.

It’s rather sad because Quickbooks could really rock if the underlying infrastructure wasn’t such a bodge job of disparate systems glued together with shady vendors who show little to no accountability for their actions.

Meanwhile, I’ve learnt my lesson…move the money out from “Green Dot Bank” as fast as possible and never trust them for anything other than receiving payments for invoices and forwarding them on to the real corporate checking account held by a real financial institution that is entirely US-based.

And should even that minimal use of them fail, I can expect zero support and accountability from either Intuit or Green Dot from processes that are designed to intentionally frustrate the hell out of the consumer rather than solve easily solved problems for them.

Meanwhile, I’ll let you know how this story ultimately ends…assuming I’m alive when it actually happens!